Modifications to Credit Rating: Insurance companies utilize credit rating to calculate insurance coverage rates in every state, although 3 states (California, Massachusetts, and Hawaii) have actually prohibited the practice. If you have a low credit rating, or if your credit rating unexpectedly dropped (state, due to personal bankruptcy), then your automobile insurance premiums could rise considerably.

This is the length of time during which an insurer can inspect your driving record. Generally, insurers utilize a lookback duration of 3 to 7 years, although lookback periods differ between insurance companies and states. California, for example, utilizes a 12-year lookback period for DUIs, while the majority of states have a 3 to 7 year lookback duration for general driving offenses.

You have actually proven experience driving securely on the road, and that indicates you're a lower risk chauffeur to insure than someone with several offenses or an accident. Make The Most Of Discounts: All insurer provide discount rates. Take benefit of bundling discounts, excellent student discount rates, security function discount rates, age-based discount rates, safe driving discounts, and other choices.

One business might give you a clean driving discount rate since you have zero accidents, for example, while another company may cancel that discount rate due to the fact that you received a speeding ticket five years ago. By comparing quotes from different insurers, you can ensure you're working with the business that finest matches your driver profile and charges you the most affordable possible rates.

How Much Does An Eye Exam Cost Without Insurance Fundamentals Explained

Consider raising your deductible to drop month-to-month premiums, for instance. Or, lower liability protection, drop collision and comprehensive coverage in older automobiles and change your policy in other methods. By executing the methods above, you can conserve money on car insurance in any state especially as a motorist with absolutely no accidents on your driving history.

As we discovered above, there are a number of factors why you could be paying excessive for car insurance coverage. Perhaps you're driving a brand name new car, for instance. Possibly you have a driving record filled with speeding tickets and traffic offenses. Possibly somebody stole your identity and abused your clean driving record.

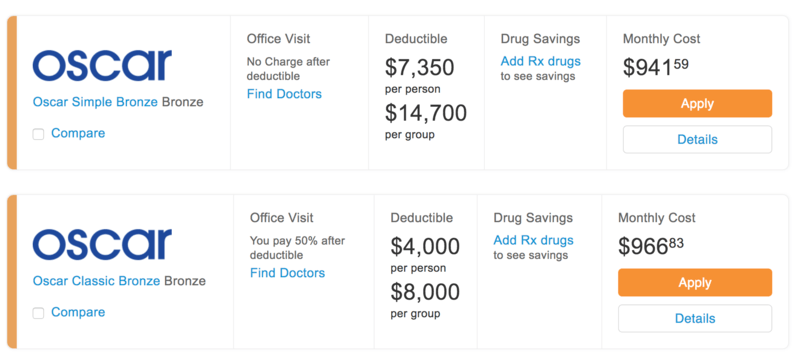

Lots of or all of the items featured here are from our partners who compensate us. This might affect which items we discuss and where and how the item appears on a page. Nevertheless, this does not affect our assessments. Our viewpoints are our own. If you're approaching your late 20s, have a great driving record and are able to buy a brand-new vehicle, you may be anticipating your automobile insurance coverage prices estimate to take a dip.

Insurance rates steadily drop through your 50s and generally start to rise again in your 60s. But there might be other reasons your rate isn't dropping a minimum of not as much as you had actually hoped. Here are some possible elements. For one, it's smart to safeguard a brand-new vehicle with thorough and crash protection, which spend for damage to your own car.

Fascination About Where Can I Go For Medical Care Without Insurance

As Detroit residents know, your ZIP code has a major influence on your vehicle insurance coverage quote. If your area or city has a high rate of crashes and car theft, you could end up paying a http://palerijfn6.nation2.com/all-about-what-is-deductible-in-health-insurance high premium through no fault of your own. Rural locals generally delight in the lowest rates, whatever else being equivalent.

Loaded with security functions as your vehicle may be, that doesn't mean it's low risk from an insurer's point of view. If the design you drive has a bad history of claims, your insurance provider will charge you appropriately. Smaller SUVs and minivans tend to garner the most affordable premiums, while chauffeurs of expensive sports cars pay the most for insurance.

If you don't pay your credit card expense, mortgage or auto loan, that will lead to a lower credit report. And if your state is one of those that enables insurance provider to use credit details in identifying your premium, your insurance coverage rates might go up substantially as much as 127% in nine cities surveyed, according to the Customer Federation of America.

But even as you get older, remaining single can have an effect on what you pay. The Chicago chauffeur with the Ford Focus might save about $10 each month by getting hitched; so could his partner. It's never fun to pay more than you anticipate for automobile insurance coverage (how to get health insurance after open enrollment). However you can prepare ahead.

How Much Does A Filling Cost Without Insurance Fundamentals Explained

Other aspects impacting your rates aren't as simple to control. Paying down large charge card financial obligations ought to improve the rates you're used, but that can take time. And packing up and transferring to a neighborhood that takes pleasure in better car insurance coverage rates isn't normally sensible. No matter where you live, however, looking around for automobile insurance will reveal whether you're getting a great price or a raw offer.

Some months, just keeping gas in the tank and remaining on top of cars and truck insurance coverage premiums can feel like an insurmountable task. If you're taking out a payday loan just to keep up with your automobile insurance, you might be questioning, 'why is my vehicle insurance so costly?' Rapidly followed by, 'how do I lower my car insurance rates?' [Read: The Finest Vehicle Insurance Business of 2020] First of all, there are known elements that can increase your insurance coverage rates.

While a few of these factors are out of your control, like age and gender, others can typically be operated in your favor. [Read: Where to Find Financial Relief Throughout the Covid-19 Pandemic] Why is my cars and truck insurance coverage high? Insurance coverage companies determine premiums based on how risky or costly they think the motorist will be.

When you get a ticket for a traffic violation, the real expense isn't as simple as paying it off and being done. These occasions enter into your driving record, where insurance provider will see them as a sign of threat. The more incidents you have on your driving record, the more expensive you will be to guarantee, and the greater your premiums will be.

Getting My How Does Whole Life Insurance Work To Work

The more claims you have actually submitted, the more likely you are to sue. This simple reasoning plays a considerable function in how an insurance company determines just how much it'll cost to guarantee you. When you have a history of filing claims, it indicates that you are most likely to have an accident and submit a claim on that accident.

Credit report are utilized by insurers to calculate the likelihood of both expense and danger. Statistically, the lower a credit history, the more likely a person is to file a claim. Conversely, the greater a credit rating, the most likely a person is to pay their premiums on time. Automobile insurance is just one of many industries that utilizes credit rating and ratings to screen their customers and determine rates.

Insurance providers see high levels of driving as a threat factor for this factor. The more often you drive, the most likely they are to be called upon for an insurance coverage claim. Consider it like this, for every mile you drive, there is some little statistical possibility that you'll have a mishap.